No products in the cart.

Financial, Investment, Working class

How To Save Money Amidst Inflation

Getting Started with Savings

Have you ever considered what actions you may do right away to improve your ability to manage your money savings in spite of the fact that inflation may have negatively impacted your finances?

Minutes to Read: 20 minutes

Age Bracket: 30-50 years old

Building your wealth is different from simply having money in the bank that you can withdraw whenever things get tough financially. You should only keep money in a savings account for daily needs and an emergency reserve; otherwise, you should think about other ways to store your money.

Continue reading to learn more about the fundamentals of inflation, what causes it, how to measure it, its benefits and drawbacks, and how to save money in the face of it. Read the entire article to have a complete understanding of inflation and interest rates. Alternatively, you can utilize the supplied links to skip to a certain section if you know what you’re searching for.

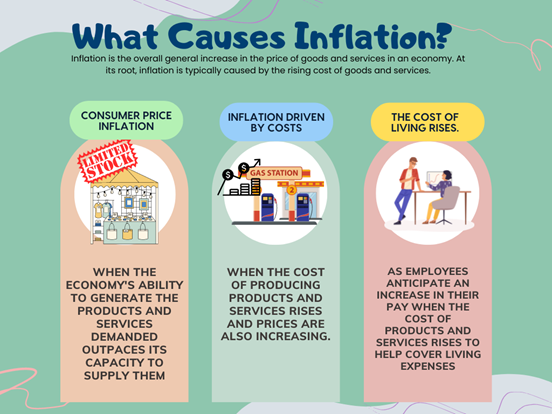

What is Inflation?

A basic explanation of inflation is that it is the widespread increase in the price of commodities throughout the economy. Rising prices for common items like milk, transportation, and fruits and vegetables may result from this. But inflation is much more complicated than it appears.

The Development Budget Coordination Committee (DBCC) reported that the national government has again raised its projection for the inflation rate in 2022, which is now from 4.5 percent to 5.5 percent. Amenah Pangandaman, the budget secretary, disclosed during a conference on July 8, 2022, that the revisions were still a result of the conflict between Russia and Ukraine and other supply issues.

A currency loses value due to inflation, which is frequently expressed as a percentage. The money in your wallet may buy less when the cost of basic products and services rises. This explains why the cost of transportation and common goods when your parents were your age was substantially lower than the cost of those same basic necessities today.

How do we measure Inflation?

The Consumer Price Index (CPI), which calculates the percentage change in the cost of a selection of products and services that families typically use, is the most well-known measure of inflation.

Consumer Price Index (CPI)

In the Philippines, the CPI is calculated by the Philippine Statistics Authority. The CPI calculates the average change in prices consumers pay over time for a market basket of goods and services. The most significant categories in the Consumer Price Index in the Philippines are housing, water, electricity, gas, and other fuels (22%), transportation, and food and non-alcoholic drinks (39% of the total weight) (8%). The index also includes recreation and culture (2%) and health (3%), as well as education (3%) and apparel and footwear (3%). (2%). The remaining 15% comprises alcoholic beverages, cigarettes, furniture, home appliances, dining establishments, and other items and services.

Inflation Formula

The basic inflation formula goes as follows:

Inflation = PriceYear 2– PriceYear 1PriceYear 1100

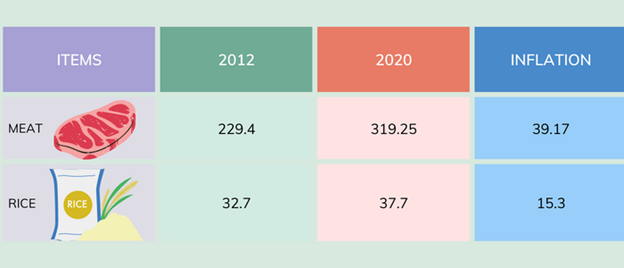

We can use an example to clarify how inflation is computed. We estimate inflation in this case for a basket that includes two items—meat and rice. The above formula can be used to determine inflation for a single item.

The price of the meat per kilogram was ₱229.4 in 2012 (Year 1) and the price increased to ₱319.25 in 2020 (Year 2). The price of rice per kilogram was ₱32.7 in 2012, and this increased to 37.7 in 2020.

The formula can be used to determine inflation for each of the individual goods.

- For meat, annual inflation was 39.17%

- For rice, annual inflation was 15.3%

However, the CPI does not represent the price level. The CPI gauges the economy’s rate of price changes, not the level of prices. It does not imply that eggs are more expensive than bread if the price index for eggs is 220 and the price index for bread is 170. It simply indicates that, as of a certain moment in time, the price of eggs has gone up higher than the price of bread.

The CPI tracks variations in product prices in the capital areas of the Philippines for practical reasons. Regional, rural, or remote places are not included in its measurement of price increases. Additionally, the CPI does not account for the variations in spending habits among various households. Because every household is unique, some may spend significantly more money on particular products than others. For instance, although cars account for almost 8% of the CPI basket, not every household owns one.

The Economy of the Philippines

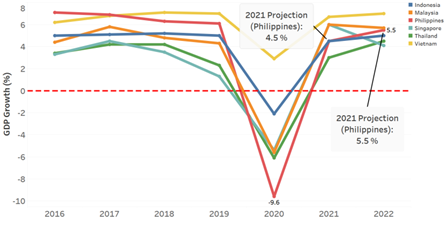

The Asian Development Outlook (ADO) 2022 Supplement says the Philippine economy will grow at least 6.5% in 2022, up from the bank’s April forecast of 6.0%. The growth projection for 2023 remains at 6.3%

Before Pandemic

Between 2010 and 2019, average yearly growth grew to 6.4% from an average of 4.5% between 2000 and 2009. A decrease in poverty rates and the Gini coefficient shows that the Philippine economy has improved in generating equitable growth. While the Gini coefficient decreased from 44.9 to 42.7 over the same period, poverty declined from 23.3% in 2015 to 16.6% in 2018.

Source: Asian Development Outlook

After the Pandemic

The Philippine economy maintained its upward trend and gained 7.7 percent in the fourth quarter of 2021, following five quarters in a run of negative growth. This raises the GDP growth rate for the entire year to 5.6 percent. The full-year reading is higher than the government’s revised projected range of 5 to 5.5 percent, which gives us even more hope for a more promising rebound.

How Banks Provide Relief From Inflation?

You should at least keep your funds growing fast enough to stay up with inflation. And with a typical savings account, you are unable to accomplish that. Thankfully, there are financial solutions available today that can increase your money more quickly than a standard savings account. Although it doesn’t yield as much as a real investment mechanism, it’s still adequate to at least stay up with the inflation that never stops.

Before we get into that, what is the interest rate and how does it work? Typically, interest rates are represented as a percentage of the principal sum. Based on the bank, it may be fixed or variable based on conventional deposit products including savings deposits, term deposits, and some demand or current accounts. Interest rates function in two different ways for the typical consumer:

- The fee associated with borrowing money.

- The amount of money earned from a deposit account or an investment

How do banks determine interest rates? The combination of the supply and demand for funds in the money market determines the level of interest rates. Prior to its complete liberalization in 1983, the Bangko Sentral ng Pilipinas (BSP) set interest rates. All bank rates, except those for short-term loans, were abolished by the Philippines’ Central Bank in 1981. With the abolition of the final short-term lending rate caps in 1983, the restructuring of bank rates was complete.

In the Philippines, interest rates are established according to a market-oriented structure, allowing any financial institution providing banking products and services to do so. This means that the interest rates that banks, lending investors, and pawnshops charge are not regulated by the BSP.

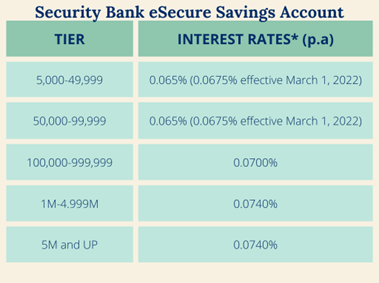

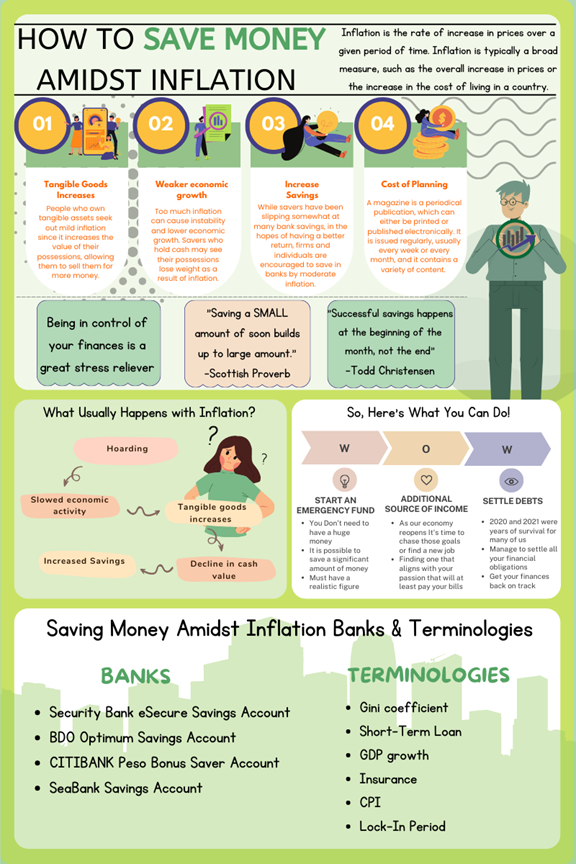

Security Bank eSecure Savings Account

- Maintaining Balance: ₱500

- Balance to Earn Interest: ₱5,000

Even if you must save ₱5,000 in order to begin receiving interest on your money, you may at least get started on your savings objectives with just ₱500.

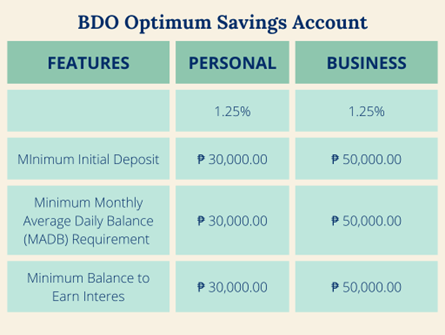

This is a savings account that BDO Unibank Inc. offers, providing their customers with a higher interest rate for doing so. However, this kind of savings account requires a larger initial deposit and has additional costs that you might want to consider. As long as you meet the initial amount criteria, the interest rate is also fixed regardless of the amount; whether this is advantageous or disadvantageous depends on your financial objectives.

Additionally, the account offers free withdrawals up to three times every month.

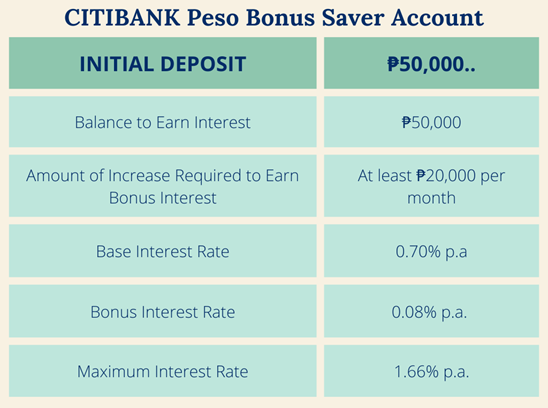

CITIBANK Peso Bonus Saver Account

This Citibank interest-bearing deposit account encourages savers to increase their savings. When depositors deposit extra money each month into the Citibank Peso Bonus Saver Account, bonus interest is added on top of the base rate.

It provides a 0.70% gross p.a. base interest rate. If your account average increases by at least 20,000 per month over a rolling 12-month period, you will be eligible for bonus interest. The maximum rate is 1.66% gross annually. Once your average balance has increased for 12 months in a row. Additionally, you get unrestricted access to free withdrawals of your money

.

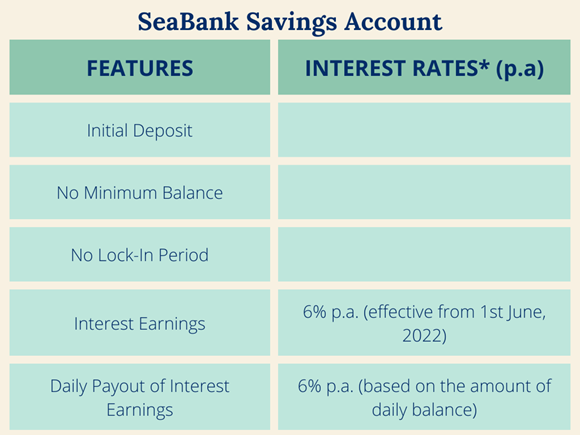

Get 6% p.a. interest accruals on any account balance, effective on June 1st, 2022. There is no lock-in period, no deposit cap, and no minimum balance requirement. The best part is that SeaBank daily credits your account with interest earnings. Moreover complimentary is your account! Account fees and online transfer costs are not charged by SeaBank. Anytime, for no cost, you can transfer money from ShopeePay to SeaBank.

What Saving Steps To Mitigate Inflation’s Impact?

Savings are depreciated by inflation from their original value. No matter how we feel about it, inflation is a fact of life. While the cost of our essentials rises, the worth of our money stays the same.

The goal is to increase your money. Ensure you already have the necessities in place, including an emergency fund, health insurance, a stable debt-to-income ratio, and most crucially, an additional budget, before you act hastily. If you’ve checked off every box, it’s reasonable to conclude that you can now diversify your finances so that you can increase its worth rather than see it decline.

Depending on the situation and how quickly prices move, inflation can be seen positively or negatively. High inflation tends to harm consumers. So let’s see the pros and cons of inflation:

Pros

- Worth of tangible goods increases

- Economic expansion

- Real wages

- Price adjustment

- Increased Saving

Cons

- Pay more money for products and services.

- Weaker economic growth

- The decline in cash value

- Slowed economic activity

- Higher unemployment rates

- Hoarding

These five financial objectives are essential to your financial well-being and may be completed in less than a year.

- Start an emergency fund

Realistically, emergency savings don’t necessarily need to equal a certain multiple of your annual salary. As long as you believe it will be enough to cover your financial demands when you need it, you can save aside as much money as you choose. To be considered to have an emergency fund, you must have at least three months’ worth of monthly expenses in it.

For starters, ₱10,000 or even ₱20,000.

Calculate all of your monthly expenses to arrive at this figure, then multiply it by the number of months you want to put money aside. Consider how much money you’d feel confident having in the bank when determining the number of months for an emergency fund. You would need to save 60,000 if, for instance, your monthly expenses are ₱20,000 and you believe that saving for three months’ worth of expenses will be the right safeguard for you.

- A new job or a new source of income are fresh starts

The objective in the current difficult economic environment is to obtain a job that will at least cover your bills. It is already a plus if you can find one that fits your enthusiasm.

Nowadays, there are many options to start a side business, particularly online. Either search for freelance work or launch your own web business.

- Pay off (at least some of) your debts

You simply need to keep working, keep track of your spending, and improve your money management. While there isn’t a magic formula for getting out of debt, there are techniques that can help you rethink how you approach managing your finances.

- Boost or establish a payment history

You can improve your payment history by using your credit card to make purchases and paying it off right away, assuming you aren’t drowning in debt. Do not wait until the due date to settle all card payments you have made. Another piece of advice is to just use your credit card for little purchases; avoid using it for expensive products because you’ll probably be tempted to break up the payment into several installments.

- Acquire insurance

If you now have insurance policies, be sure to see them through to the end because we never know when they will come in handy. Make it a point to obtain insurance if you don’t already have one; the earlier you do so, the better. You’ll not only pay less but the process will be completed sooner, giving you more time to prepare for any changes in your insurance needs.

In the meantime, be sure to pay your SSS and Philhealth contributions on time each month. Although these public insurance programs might not be as lucrative as private insurance, you can never have too much assistance or insurance when you need it.

This article explains the fundamentals of inflation, what causes it, how to measure it, its benefits and drawbacks, and how to save money in the face of it.

Terminologies that You should know:

- Gini coefficient – The Gini coefficient (Gini index or Gini ratio) is a statistical measure of economic inequality in a population.

- A Short-Term Loan – is a type of loan that is obtained to support a temporary personal or business capital need.

- Market-Oriented Structure – an approach means a business reacts to what customers want. The decisions taken are based on information about customers’ needs and wants, rather than what the business thinks is right for the customer.

- GDP growth – measures how fast the economy is growing.

- CPI – The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

- Insurance – is a contract in which an insurer indemnifies another against losses from specific contingencies or perils.

- SSS – The Social Security System (SSS) administers social security protection to workers in the private sector. Social security provides replacement income for workers in times of death, disability, sickness, maternity, and old age.

- Philhealth – PhilHealth is a government-owned and controlled corporation and is the country’s national health insurance provider. It gives all of our private employees health coverage thanks to the contributions we make that are acquired by automatically deducting a certain percentage from our salaries.

- Contributions – the act of contributing: such as. a : the giving or supplying of something (such as money or time) as a part or share They’re collecting donations for contribution to the scholarship fund.

- Lock-In Period – this is the time period for which the investment or the invested amount cannot be withdrawn or sold.

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

Credit Card Starter Guide for Beginners

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.