Skip to content

Skip to contentNo products in the cart.

Financial, Millennial, Working class

Pag-IBIG Housing Loans; Step-by-step guide on how to apply

Things You Need to Know About Pag-IBIG Housing Loans

Are you saving up for your dream home? I’m pretty sure that will take some time. If you’re a Filipino Employee, chances are, a part of your salary is deducted to be contributed to the Pag-IBIG Funds. The most significant advantage of being a member of Pag-IBIG is their Housing Loans. Of course, nothing beats the feeling and the sense of fulfillment when you see your name on land and house title.

Minutes to Read: 10 minutes

Age Bracket: 26 – 40 years old

Acquiring a house requires a lot of time and work, just like everything else. Researching and finding which loan is suitable for you may be stressful; however, if you find yourself reading this article. Who might know? Maybe Pag-IBIG Housing Loans is for you! If that’s the case, I’ve listed everything you need to know to apply for a housing loan in Pag-IBIG.

Pag-IBIG Housing Loans

Pagtutulungan sa Kinabukasan: Ikas, Bangko, Industriya, at Gobyerno, commonly known as Pag-IBIG, is a joint private and government personnel fund that addresses the country’s need for a national savings program and to finance and help Filipino workers to avail affordable shelter. The Pag-IBIG Fund was established under Presidential Decree No. 1530 on June 11, 1978.

Furthermore, on December 14, 1980, Pag-IBIG became independent from NHFMC with the signing of PD 1752. With PD 1752, all SSS and GSIS member-employees are now required to be Pag-IBIG members.

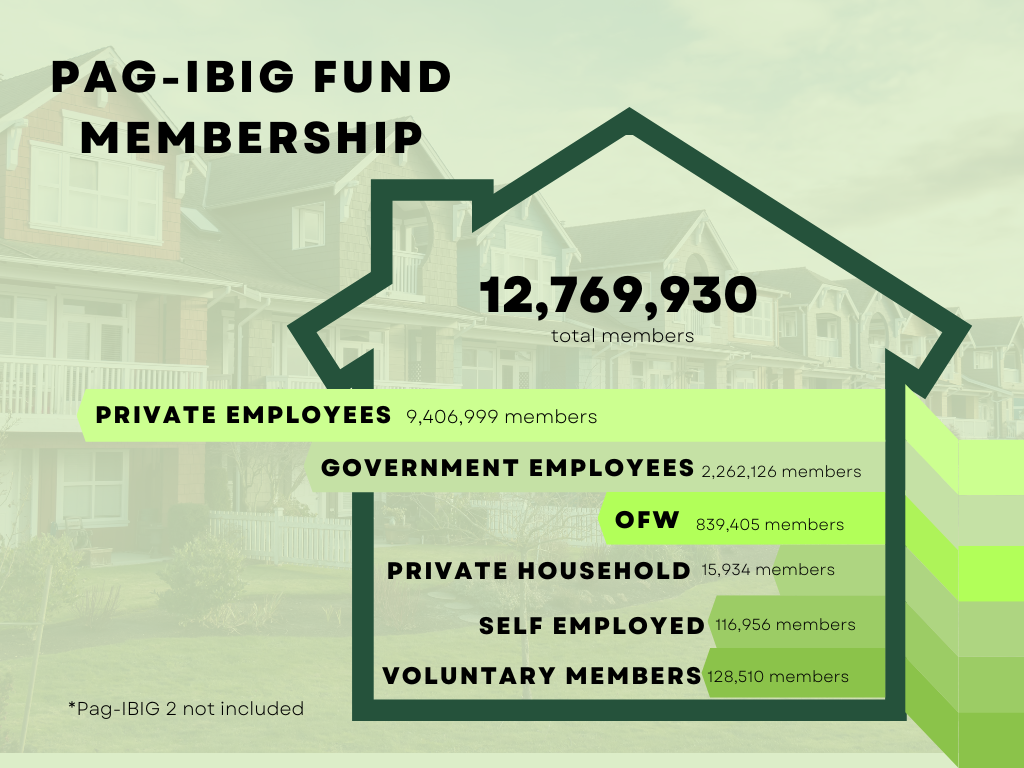

According to Pag-IBIG 2020 annual report, the Pag-IBIG Fund’s membership consists of 9,406,999 private employees, 2,262,126 government employees, 839,405 overseas Filipino workers, 15,934 private households, 116, 956 self-employed Filipinos, and 128,510 voluntary members.

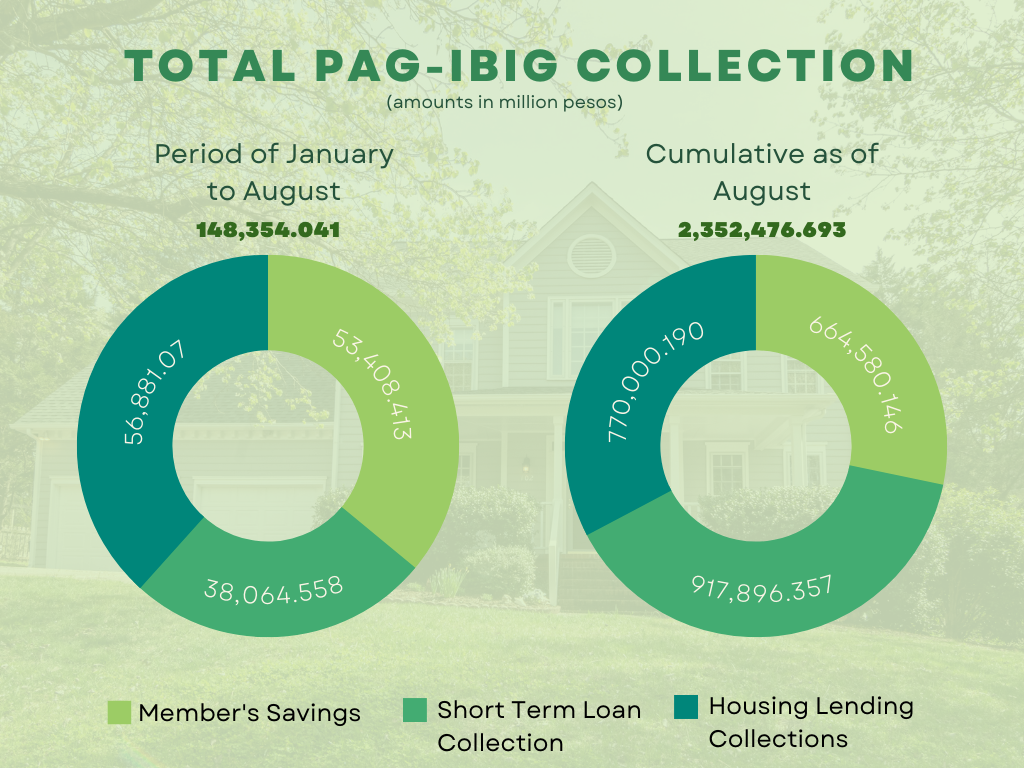

From January to August 2022, the total collection of savings is ₱148 million and an amount of ₱2.352 billion cumulative as of August 2022. The housing loan or wholesale home lending collection in that amount is ₱770 million.

The Pag-IBIG Housing Loans offer up to ₱6 million loanable amount with a low fixed period interest rate. These housing loans also come with insurance such as Mortgage Redemption Insurance (MRI), Sales Redemption Insurance (SRI), or Fire and Applied Perils Insurance (FAPI), whichever is applicable. You can use your housing loan to finance your plans for your dream house, such as

- Purchasing a fully developed residential or adjoining residentials not exceeding 1,000

- Purchasing a residential house and lot, townhouse, or a condominium unit.

- Construction of your residential unit on your residential lot

- Financing your home improvement

- Financing your existing house loan if you regularly pay your loan’s amortization without any payment made beyond thirty (30) days past due for the last six (6) months from the date of the application.

It has a maximum loan repayment term of thirty (30) years. However, your age should not exceed seventy (70).

In terms of loan interest rates, Pag-IBIG offers fixed interest rates for up to thirty (30) years. This means that you will be paying a constant amount of monthly amortization at a given period, depending on what you chose. After the fixed interest rate period you have chosen, a viable rate that varies from the market’s interest rate change will be applied to your loan.

| Pag-IBIG Housing Loan Fixed Interest Rate | |

| 1 year 5.750%

3 years 6.375%

5 years 6.625%

10 years 7.375%

15 years 8.000%

20 years 8.625%

25 years 9.375%

30 years 10.000% | |

Pag-Ibig Membership

To experience the benefits of being a Pag-IBIG member, you must be a member first! If you’re interested in becoming one, you should know that this can be mandatory if you are employed and voluntary if you’re self-employed or non-working, depending on your employment status. Here is the list of who can become a Pag-IBIG member.

Who can apply for Pag-IBIG Membership?

1. Mandatory Membership

Under the Home Development Mutual Fund Law of 2009, membership in the Pag-IBIG fund became mandatory for all Filipino and foreign-based employees.

- Private Employees

- Government Employees

- Overseas Filipino Workers

- Self-Employed Professionals

- House Maid / Kasambahay

2. Voluntary Membership

Pag-IBIG Membership is not only for Filipino Employees. It is open to all Filipinos and Foreign residents (who have resided in the Philippines for at least six months) aged 18 to 65.

- Non-working Spouse

- Former Pag-IBIG Members

- Baranggay Officials

- Expatriates

- Students

- Unemployed Filipinos

- Overseas Filipino Immigrants

- Others

Pag-IBIG Registration

If you fall in one of the categories above, you are eligible to register for Pag-IBIG Fund, which is now available online! This is for individuals who will register as a new member and have never been issued a Pag-IBIG Membership ID (MID) number. However, if you have already tried registering online, you cannot try it again.

Employees are not required to register online since their employers will do it for them. Your HR will ask for your personal information so they can work on your Pag-IBIG membership and submit it to the Pag-IBIG fund and other government agencies. Otherwise, here are the steps to register with Pag-IBIG Online.

Steps to Register with Pag-IBIG Online

1. Visit the Pag-IBIG Fund Online Registration System – use the latest version of your browser to ensure fast transactions and avoid issues when registering.

2. Fill up the Pre-Registration form – enter all the needed information on your screen. Before submitting, type the code on your screen and click “Submit” once done.

3. Fill out the Online Membership Registration Form – after the Pre-Registration form, you will be redirected to Pag-IBIG’s Online Membership Registration Form. The form has eight (8) tabs you must fill out with different types of information, such as

3. Fill out the Online Membership Registration Form – after the Pre-Registration form, you will be redirected to Pag-IBIG’s Online Membership Registration Form. The form has eight (8) tabs you must fill out with different types of information, such as

- Member Info

- Other Info

- Address

- Contacts

- Heirs

- Member Category

- Employment History

- Summary

Note that fields that have red asterisks (*) are required and not allowed to leave it blank. You have to fill out the field before proceeding to the next page. Once you’re done filling a tab, click the “Next” button to proceed to the next page. If you have to edit information from the previous page, click the “Back” button to go to the previous tab

4. Print your Member’s Data Form (MDF) – your MDF is your proof of Pag-IBIG Registration containing your Registration Tracking Number (RTN), also called Pag-IBIG Tracking Number. You can use this to pay your contributions while waiting for your permanent Pag-IBIG Number.

Pag-IBIG Member’s Data Form (MDF)

5. Request for a Permanent Pag-IBIG Number – You can request your permanent Pag-IBIG Number after two working days via SMS. Just send a text message in this format IDSTAT RTN BIRTHDATE (MM/DD/YYYY) (Example IDSTAT 912365478925 03/08/1981) and send it to any of these numbers:

Globe and TM: (0917) 888-4363

Smart, TNT, and Sun: (0918) 898-4363

You can also call the Pag-IBIG Hotline : 724-4244 to inquire and ask for your permanent Pag-IBIG Number. Take note of your RTN since the customer agent will ask for it.

Pag-IBIG Contribution

Maybe you’re wondering how much you should contribute to your Pag-IBIG. If you are, I have listed below the monthly contributions to the Pag-IBIG fund, depending on your current employment status. Scroll down and find which applies to you.

1. Filipino Employee

If you are a Filipino Employee, your monthly Pag-IBIG contributions are shared with your employer.

Your monthly Pag-IBIg contribution is automatically deducted from your monthly salary. If you earn less than ₱1,500 monthly, 1% of your salary will be deducted. If you’re making more than ₱1,500, 2% of your basic salary will be deducted as your monthly contribution.

Additionally, your employer will pay their share of the contribution of 2% of your salary, which will not be deducted from your paycheck.

Use the formula to see how much you and your employer will pay.

Pag-IBIG Contribution = Your monthly salary x Contribution Rate

The Maximum salary used in computing your monthly contribution if your salary is more than ₱1,500 is ₱5,000. To illustrate this, suppose your monthly salary is ₱10,000. This means if you calculate your monthly contribution, we will be using ₱5,000 as your salary, and you will pay 2% of it as your monthly Pag-IBIG contribution and 2% from your employer. Thus,

₱5,000 x 0.02 = 100 (Your contribution)

₱5,000 x 0.02 = 100 (Your employer’s contribution)

Therefore, an amount of ₱100 will be deducted from your salary while your employer adds ₱100 to your monthly Pag-IBIG contribution. You now have a total of ₱200 monthly contributions.

| Your Monthly Salary | Your Contribution Rate | Your Employer’s Rate | Total Monthly Contribution Rate |

| At least ₱1,500 | 1% | 2% | 3% |

| More than ₱1,500 | 2% | 2% | 4% |

2. Overseas Filipino Workers

Being an Overseas Filipino worker means you are also required to be a Pag-IBIG member and have to pay your monthly contributions. If your employer is subjected to the Pag-IBIG coverage, the same rates per monthly salary apply to you from the table above since you are an employee.

However, if your employee is exempted from the Pag-IBIG coverage and your monthly salary is above ₱1,500, you’re required to pay 2% of your monthly salary, with ₱5,000 as your maximum monthly salary used for computing your monthly contribution, which means you have to pay at least ₱100 as your monthly Pag-IBIG contribution.

If you’re planning to avail the Pag-IBIG Housing Loans in the future, it is advisable to pay your employer’s 2% part of the contribution. You will have a total of ₱200 monthly contribution.

| Your Monthly Salary | Your Contribution Rate | Your Employer’s Part Rate (Optional; if planning to avail Housing Loan in the future) |

| More than ₱1,500 | 2% | 2% |

To show you your monthly contribution, the same formula applies here. Suppose your income is ₱30,000; we will still use ₱5,000 as your monthly income for the computation since that is the maximum amount used in Pag-IBIG. Thus,

₱5,000 x 0.02 = ₱100 (Your contribution)

₱5,000 x 0.02 = ₱100 (Optional).

Therefore, you will be paying at least an amount of ₱100, but has an option to pay ₱200 if you prefer.

3. Self-Employed Members

Unlike employed individuals whose employers shoulder half their monthly contribution, self-employed members pay their full monthly contribution by themselves.

Those who earn less than ₱1,500 have to pay 1% of their monthly income, while those who earn more than ₱1,500 have to pay 2% of their monthly income. Similar to the computations above, the maximum monthly income limit used to calculate the contribution is ₱5,000.

To illustrate the calculation, suppose you earn at least ₱5,000 a month. Thus,

₱5,000 x 0.02 = ₱100 (Your contribution)

Therefore, you should pay at least ₱100 as your monthly Pag-IBIG contribution. However, you can also pay an additional ₱100 or higher if you’re planning to get the Pag-IBIG Housing Loans in the future.

| Your Monthly Income | Your Contribution Rate | Optional Contribution |

| Less than ₱1,500 | 1% | |

| More than ₱1,500 | 2% | ₱100 (or higher) |

4. Kasambahay or Housemaid

If you are a kasambahay or a housemaid in the Philippines, you don’t have to worry about paying your monthly Pag-IBIG contribution since your employers will shoulder your full monthly contribution unless your income is more than ₱5,000.

And If you are earning less than ₱1,500, your employer will pay 3% of your monthly salary. If your salary ranges from ₱1,500 to ₱4,999, your employer will pay 4% of your contribution rate. However, if you’re earning more than ₱5,000, you will be paying 2% of your monthly income while your employer pays the other 2%.

To show the computations, suppose you earn ₱4,000 per month. This means your employer will shoulder your full 4% monthly contribution rate. Thus,

₱4,000 x 0.04 = ₱160 (Your contribution paid by your employer).

Therefore, you have a total Pag-IBIG monthly savings of ₱160.

| Your Monthly Salary | Your Contribution Rate | Your Employer’s Rate |

| Less than ₱1,500 | 0% | 3% |

| Between ₱1,500 and ₱4,999 | 0% | 4% |

| More than ₱5,000 | 2% | 2% |

5. Non-working Spouse

If you fall into this category, your monthly contribution is based on half of your working spouse’s salary. When half of your spouse’s monthly salary is below ₱1,500, you will be paying 1%, while you’ll pay 2% of your spouse’s half salary.

To illustrate this, suppose you are a full-time housewife with a spouse who earns ₱5,000 per month. Half of ₱5,000 will be ₱2,500. This means that this falls below the rate of 2%. Thus,

(Your spouse’s salary/2) x contribution rate = Pag-IBIG Contribution

(₱5,000/2) x 0.02 = ₱50 (your monthly contribution).

Therefore, you have a total amount of ₱50 Pag-IBIG monthly savings.

| Half of your spouse’s salary | Your Contribution Rate |

| Less than ₱1,500 | 1% |

| More than ₱1,500 | 2% |

Qualifications and Requirements

To qualify for the Pag-IBIG Housing Loans, you should satisfy their basic qualifications requirement before applying for the loan.

Qualifications

- You should have at least twenty-four (24) monthly membership savings

- You should not be above 65 years old when you apply for the loan and not be more than 70 years old at the maturity of the loan

- Legal capacity to encumber real property

- Should have the ability to pass background checks/credit and employment/business checks of Pag-IBIG Fund.

- Has no outstanding Pag-IBIG Short Term Loan (STL) at the time of the application

- Has no foreclosed, canceled, bought back due to default, or subjected due to dacion en pago Pag-IBIG Housing Loan.

- You must update your account if you have an existing Pag-IBIG Housing Loan.

If you fit right into all the qualification requirements stated above, then you’re qualified to apply for the loan! However, aside from satisfying their qualification requirements, there are documents that you should prepare when applying. Ensure all required documentation is complete and accurate when submitting your application to ensure a fast process and avoid delays.

Requirements

- Housing Loan Application with your recent ID photo or co-borrower (If applicable)

- Your proof of income

- A photocopy of one (1) valid ID of the Principal borrower and spouse, or co-borrower and spouse

- Latest and Certified True Copy of the Transfer Certificate of the Title (TCT)

- If condominium unit, present TCT and certified true copy of the Condominium Certificate of Title (CCT)

- Updated tax declaration (house and lot) and a photocopy of the Updated Real Estate Tax Receipt

- Vicinity map or sketch map of the property

- Additional Requirements by Loan purpose

How to Apply?

We have now discussed all the essential information you must know before applying for a loan. Now that you’re prepared with all the knowledge you have read above, we will discuss the steps you must follow to apply for a Pag-IBIG Housing Loan.

Steps to Apply for a Pag-IBIG Housing Loan

- Prepare all the required documents.

Preparing is essential when applying for a loan. Make sure all the documents needed are complete and accurate before submitting. It is best to make a checklist of all the requirements you need (stated above) to ensure you did not forget anything.

- Submit your Loan Application.

Once all of your requirements are prepared, you can now submit your loan application. You can submit your application form and initial requirements online via Virtual Pag-IBIG. You can also bring your application form and your complete set of requirements to a Pag-IBIG Housing Business Center or Pag-IBIG Fund Branch near you. Click here to see the entire directory of all the branches and centers to find the nearest one to you. Upon submission of your requirements, you have to pay a non-refundable fee worth ₱1,000.

- Wait for your Notice of Approval (NOA) and Letter of Guarantee (LOG).

Once your loan application is approved, you will receive your Notice of Approval and Letter of Guarantee. This will only be released to the borrower; if the borrower is an OFW, their attorney will receive it on their behalf. However, if your loan application is rejected, you will receive a Notice of Disapproval instead.

- Complete all your NOA requirements.

Besides signing your loan documents, you must complete all the requirements in your Notice of Approval. You have ninety (90) calendar days to gather all the requirements that you need, which include the transfer of the title, annotation of mortgage, Bureau of Internal Revenue for payment of capital gains tax and documentary stamps, and lastly, Local government unit for payment of transfer tax, and transfer of tax declaration.

- Receive your Housing Loan Proceeds

Ten (10) days after submitting your post-approval requirements, you will be notified to receive your housing loan proceeds and the guidelines on how the proceeds will be released conveniently. To receive your loan proceeds, you must bring at least two (2) valid IDs and documents related to receiving your loan proceeds, such as the assignment of loan proceeds and the Deed of Absolute Sale with the original stamp from the registry of deeds. If you won’t be paying your loan through salary deduction, you must bring 12 postdated checks.

- Start paying your loan’s monthly amortization.

One (1) month after your loan proceeds are released, you will start paying the monthly amortization of your Pag-IBIG Housing Loan. To know the estimated amount of your monthly amortization, you can use their Pag-IBIG Housing Loan Affordability Calculator. Just input all the necessary information needed, and you will see the monthly amortization you must pay. Always take note of your permanent Housing Loan Account Number when paying. You may pay through various accredited collecting partners nationwide or online payment facilities. You can also pay online via Virtual Pag-IBIG for your convenience.

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.