No products in the cart.

Family And Children, Financial, Millennial, SSS Updates, Working class

Social Security System (SSS): A Comprehensive Guide to Loans Offered

Top 5 SSS Loans You Can Apply To

Making both ends meet is a struggle amidst the pandemic in the Philippines. COVID has affected everyone’s finances, and looking for another source of income is difficult. Being an employee in the Philippines requires you to become an SSS member, where an amount is automatically deducted from your monthly salary. The good thing is that one of the perks of being an SSS member allows you to apply for their loan offers quickly and conveniently whenever you’re short on your finances.

Minutes to Read: 8 minutes

Age Bracket: 26 – 40 years old

SSS is commonly known for its retirement income benefits. Aside from this, there’s a whole lot more that SSS can offer and provide, one of which is its loan offers. To know more about the said loan offers, read more!

What is SSS?

Social Security System, commonly known as SSS, is a government financial institution located on East Avenue, Quezon City, Philippines. It was established on the 1st of September 1957 through the Social Security Act 1954 and the Republic Act (RA) No. 11199, known as the “Social Security Act of 2018” or the SSS Law, effective from March 5, 2019, which protects private employees. They finance income replacement for workers in times of old age, sickness, disability, maternity, and death. The coverage and benefits offered by SSS are enhanced and expanded through various laws.

It is also a social insurance program designed to provide financial help to its members and beneficiaries, and they are qualified to apply for different loans offered by SSS. Your monthly SSS contribution is deducted from your monthly salary; where your employer will shoulder 7.37% of your salary as your contribution, and 3.63% will be shouldered by you, with a total of 11% of your monthly income will be your monthly SSS contribution which will range between ₱120 to ₱2,400 depending on your salary.

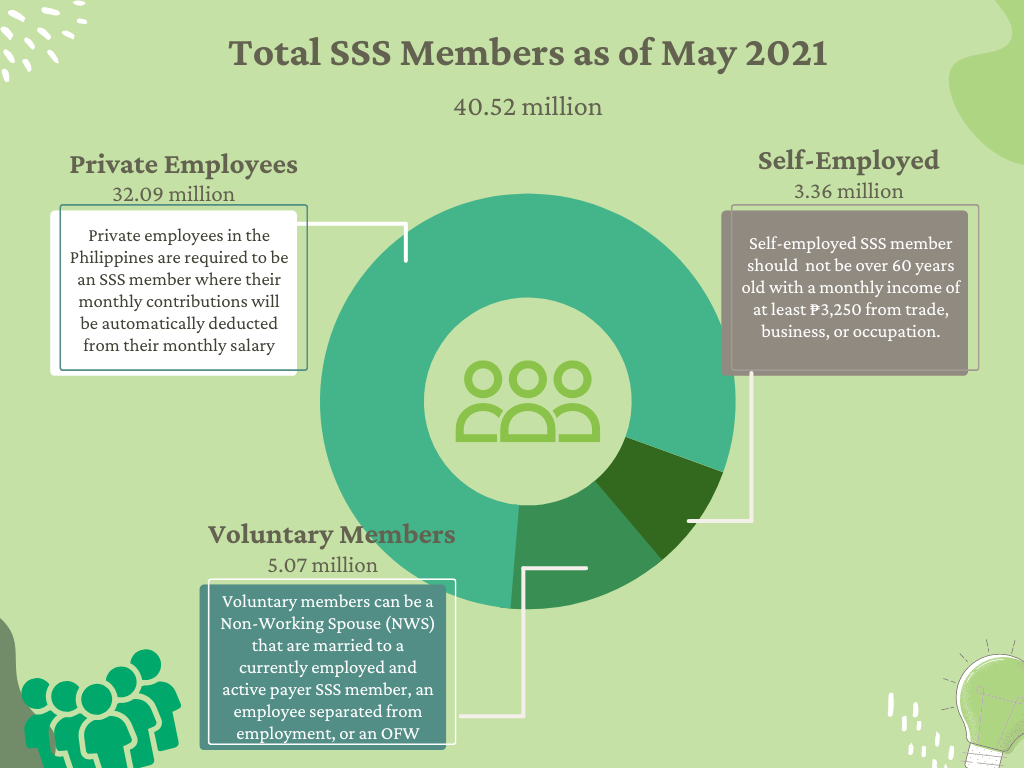

Since the Philippines’ private employees are typical members of SSS, self-employed and voluntary individuals are also allowed to apply for SSS membership. As of May 2021, there are 40.52 million SSS members, 8.3% (3.36 million) are self-employed, and 12.5% (5.07 million) are voluntary members.

Salary Loan

A salary loan can be availed by an employed SSS member or an active self-employed and/or voluntary member. It provides financial assistance to those in need and is short of cash in times of need. Members can apply for a one-month / two-month loan with a loanable amount of the member’s average / twice the average last twelve (12) monthly salary credits, or the amount the member applied for, whichever is lower.

The interest rate charged on loan is ten percent (10%) per annum until the loan is fully paid and shall be amortized for 24 months. If the member fails to pay the loan at the end of its term, interest will be continuously charged, and penalties will be added to the loan’s outstanding balance until it is fully paid.

If the loan defaults, SSS will deduct the unpaid loan amount from the member’s future long-term benefit claim. In cases where the member wants to renew the loan, this can be done once the loaned amount is already paid at its fifty percent (50%) and at least fifty percent (50%) of the loan term has passed.

Qualifications

To qualify for the SSS Salary Loan, you must:

- Be an employed active member of SSS with updated payments of other loans with SSS

- If employed, your employer must be updated with the payments of the contributions and loans.

- If not employed, must be currently paying self-employed or voluntary member.

- If planning to apply for the one-month loan, you should have thirty-six (36) monthly contributions, six (6) of which should’ve been posted in the last twelve (12) months before the application.

- If planning to apply for the two-month loan, you should have seventy-two (72) monthly contributions, six (6) of which should’ve been posted in the last twelve (12) months before the application.

Housing Loan for Repairs and/or Improvements

The housing loan offered by SSS is available directly from SSS or through its accredited financial institutions. The loan can be used for house repairs and/or house improvements. It also comes with Mortgage Redemption Insurance and Fire Insurance, where the borrower shoulders the insurance premiums.

The maximum loanable amount is ₱ 1 million, which depends on the appraised value of the collateral of at least seventy percent (70%) but will not exceed ninety percent (90%), the borrower’s capacity to pay, and the borrower’s actual need based on the contract and bills of materials evaluated by the SSS.

The loan amount will incur an interest rate of nine percent (9%) per annum with a payment term of multiples of five (5) years up to a maximum period of twenty (20) years, except for OFW members, which have a maximum payment term of fifteen (15) years. The loan’s payment term will also be subject to the principal borrower’s age, which should not exceed the age of sixty-five (65) years at the time of loan maturity and should not exceed the economic life of the house after the repairs/improvements determined by the SSS appraiser.

In terms of the loan’s collateral, acceptable collateral will be the Transfer Certificate of Title (TCT)/Original Certificate of Title (OCT) /Condominium Certificate Title (CCT) registered under the Torrens System issued by the Registry Deeds. The titles should be under the Principal Borrower’s name and/or his spouse, free from liens and encumbrances.

Qualifications

To qualify for the SSS Housing Loan, the principal borrower must be:

- An active SSS member with at least thirty-six (36) months of contributions and twenty-four (24) contributions before the application.

- The age should not exceed sixty (60) years at the time of the application.

- Should have no previous repair/improvement loan granted by the SSS or NHFMC.

- Should not be granted final SSS benefits.

- The borrower and spouse must be updated with their SSS loan(s) payments.

Direct Housing Loan Facility for Workers’ Organization Members

Workers’ Organization Members, or WOMs, is an association of employees working in the private sector registered in DOLE, the Securities and Exchange Commission, or the Cooperative Development Authority. SSS offers direct housing loans for workers or bona fide members of WOMs to afford socialized and low-cost housing. Borrowers can use the housing loan to construct a new house or dwelling unit on a lot owned by the principal borrower, to purchase a lot and construct a new home, or to purchase an existing residential unit. The loan will also come with Mortgage Redemption Insurance, Fire Insurance, and Home Guaranty Corporation Coverage, where the borrower will shoulder the insurance premiums.

The maximum loanable amount is ₱2 million, where the loan amount that SSS will grant is based on the appraised value of the collateral of at least seventy percent (70%) but will not exceed ninety percent (90%), the principal borrower’s capacity to pay, and the borrower’s actual need based on the contract and bill of materials evaluated by SSS.

If the borrower is planning to avail of the socialized housing loan, the maximum loanable amount will be ₱450,000. However, if the borrower intends to avail of the Low-cost housing loan, the loan amount ranges between ₱450,000 – ₱1 million, ₱1 million – ₱1.5 million, and ₱1.5 million – ₱2 million.

| Housing Loan Type | Loanable Amount |

| Socialized Housing Loan | Maximum of ₱450,000. |

| Low-cost Housing Loan | From ₱450,000 up to ₱1 million ₱1 million up to ₱1.5 million From ₱1.5 million up to ₱2 million |

Borrowers can combine their loanable amount limits up to a maximum of three (3) qualified SSS members provided that they are related within the first (1st) civil degree of consanguinity or affinity.

The loan is payable for a term multiple of five (5) years up to a maximum of thirty (30) years which is subject to the Principal Borrower’s age which should not exceed the age of sixty-five (65) years old at the time of loan maturity and should not exceed the economic life of the building determined by the SSS appraiser. Regarding the loan’s interest rate, refer to the table below.

| Loanable Amount | Interest Rate per Annum |

| Maximum of ₱450,000 | 8% |

| From ₱450,000 up to ₱1 million | 9% |

| ₱1 million up to ₱1.5 million | 10% |

| From ₱1.5 million up to ₱2 million | 11% |

Acceptable loan collaterals for the direct housing loans is the property covered by a Transfer Certificate of Title (TCT)/Original Certificate of Title (OCT) /Condominium Certificate Title (CCT) issued by the Registry Deeds. The titles should be under the Principal Borrower’s name and/or his spouse, free from liens and encumbrances. In cases where the loan will be used to purchase an existing residential condominium unit before actual construction (pre-selling), other residential properties acceptable to SSS can be used as collateral to secure the loan.

Qualifications

The borrower is qualified to avail of the SSS Direct Housing loan if he is:

- A bona fide SSS member registered in a workers’ organization in the private sector.

- Should have at least thirty-six (36) months of premium contribution and twenty-four (24) continuous contributions before the application.

- Borrower’s age should not exceed the age of sixty (60) at the time of the application and must be insurable.

- If the borrower’s age is sixty (60) at the time of application, the maximum loan term will be five (5) years.

- Should not have granted any previous Housing loans from SSS.

- Should not have been granted by final SSS benefits.

- The Borrower and spouse’s payments should be updated on the other SSS loan(s)

Direct Housing Loan Facility for OFWs

OFWs working in the private sector who are Filipino nationals but are now citizens or immigrants in another country, currently deployed under contract, or long-term resident overseas Filipino can avail of the SSS Direct Housing Loan. It is designed for OFWs who wish to purchase a home for themselves or their families in the country.SSS offered the direct housing loan program to help and support the government’s shelter program that aims to provide financial assistance to OFWs to purchase socialized and low-cost housing.

The maximum loanable amount is ₱2 million, where the loan amount that SSS will grant is based on the appraised value of the collateral of at least seventy percent (70%) but will not exceed ninety percent (90%), the principal borrower’s capacity to pay, and the borrower’s actual need based on the contract and bill of materials evaluated by SSS.

If the borrower is planning to avail of the socialized housing loan, the maximum loanable amount will be ₱450,000. However, if the borrower intends to avail of the Low-cost housing loan, the loan amount ranges between ₱450,000 – ₱1 million, ₱1 million – ₱1.5 million, and ₱1.5 million – ₱2 million.

| Housing Loan Type | Loanable Amount |

| Socialized Housing Loan | Maximum of ₱450,000. |

| Low-cost Housing Loan | From ₱450,000 up to ₱1 million ₱1 million up to ₱1.5 million From ₱1.5 million up to ₱2 million |

Borrowers can combine their loanable amount limits up to a maximum of three (3) qualified SSS members provided that they are related within the first (1st) civil degree of consanguinity or affinity.

The loan is payable for a term multiple of five (5) years up to a maximum of fifteen (15) years which is subject to the Principal Borrower’s age which should not exceed the age of sixty-five (65) years old at the time of loan maturity and should not exceed the economic life of the building determined by the SSS appraiser.

Regarding the loan’s interest rate, refer to the table below.

| Loanable Amount | Interest Rate per Annum |

| Maximum of ₱450,000 | 8% |

| From ₱450,000 up to ₱1 million | 9% |

| ₱1 million up to ₱1.5 million | 10% |

| From ₱1.5 million up to ₱2 million | 11% |

Acceptable loan collaterals for the direct housing loans are the property covered by a Transfer Certificate of Title (TCT)/Original Certificate of Title (OCT) /Condominium Certificate Title (CCT) issued by the Registry Deeds. The titles should be under the Principal Borrower’s name and/or his spouse, free from liens and encumbrances. In cases where the loan will be used to purchase an existing residential condominium unit before actual construction (pre-selling), other residential properties acceptable to SSS can be used as collateral to secure the loan.

Qualifications

An OFW is qualified to apply for the SSS Direct Housing Loans if he meets the following requirements:

- A certified Overseas Filipino Worker

- An OFW that is a voluntary SSS member

- Should have at least thirty-six (36) months of contribution and twenty-four (24) continuous contributions before the application

- Borrower’s age should not exceed the age of sixty (60) at the time of the application and must be insurable.

- If the borrower’s age exceeds sixty (60) at the time of the application, the maximum loan term will be five (5) years.

- Should not have granted any previous Housing loans from SSS.

- Should not have been granted final SSS benefits.

- The Borrower and spouse’s payments of the other SSS loan(s) should be updated.

Calamity Loan Assistance Program

Declared by the National Disaster Risk Reduction and Management Council (NDRRMC), the Social Security System (SSS) opened the Calamity Loan Assistance Program (CLAP) as part of the Calamity Assistance Package to all the bonafide members of SSS that is in need of financial assistance due to the effect of calamities in the country.

The loanable amount under the Calamity Loan Assistance Program is the member’s one month salary credit (MSC) computed based on the average of their last twelve (12) monthly salary credit rounded up to the nearest thousand or the amount the borrower applied for, whichever is lower.

An interest rate of ten percent (10%) per annum will incur in the loan payable in equal monthly installments for twenty-four (24) months or two (2) years. Additionally, the service fee of one percent (1%) of the loan amount is waived.

Interested applicants may apply to their My.SSS account. Once the application is approved, the loan proceeds will be credited to the member-borrower’s account, which can be found on their My.SSS Account. After receiving the loan proceeds, the first loan amortization will start two months after the loan approval. The payment’s deadline is every last day of the month; in cases where it falls on a weekend or holiday, payment can be made the next working day. Late payments will incur 1% penalty per month.

Qualifications

Affected members who are interested in applying for CLAP must meet the following requirements:

- Should have a My.SSS account ,which can be made at sss.gov.ph

- Should have at least thirty-six (36) monthly contributions, six (6) should be posted within the last twelve (12) months before the month of the application.

- Should be a resident in a calamity-stricken area declared by the NDRRMC and suffered damage and/or loss of their properties.

- Should not have been granted any final SSS benefit

- Should have no outstanding Loan Restructuring Program (LRP) or CLAP

- If the borrower is employed, his/her employer must certify the CLAP application through online My.SSS Facility

Loans are always available to those in need. Research and see what is the best fit for your needs. If you need more information and need an answer to your query, visit https://www.sss.gov.ph/

READ MORE AND SHARE!

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.