No products in the cart.

Financial, Working class

Mutual Fund: Everything You Need to Know & Its Powerful Advantages

A mutual fund is a company that pools funds from numerous sources and invests them in securities such as stocks, bonds, and payday loans. The portfolio of a mutual fund refers to all of its investments. Investors purchase shares of mutual funds. Each share reflects a shareholder’s ownership interest in the fund and the revenue it produces.Mutual fund investing is for you if your reasons for investing are diversification, convenience, and lower costs.

Mins to Read: 13 minutes

Age: 18-60 years old

Here are essential pieces of information about Mutual Funds in the Philippines:

What is a Mutual Fund?

A mutual fund is a business that receives funds from many participants and then distributes them among various investment opportunities, including equities, bonds, money market instruments, and others.

If holding stocks enables you to purchase a portion of a company, investing in mutual funds allows you to choose a basket of shares purchased from many companies. This indicates that you are not the actual owner of the company’s shares. Instead, you are a shareholder in the Mutual Fund.

Additionally, unlike stocks, you are not required to make your own investment decisions. Employed by mutual funds, fund managers oversee the funds.

Stock market investing is like grabbing a basket and stuffing it full of apples, oranges, and lemons (stocks). Each piece of fruit you put in becomes your own once you pay for it at the register.

The same analogy might play out with mutual funds:

You and your fellow consumers give your money to a “Fruit Manager,” who decides and selects which fruits to purchase. Each person has their own “portion” of each fruit in the basket. As a result, rather than keeping an entire apple to yourself, you can share a “bite” of it with others. In addition, numerous other fruit “bite” pieces were put inside the basket.

Types of Mutual Funds

Take a look at the various sorts of mutual funds now that you have a basic idea of how they operate.

1. Stock/Equity Funds

Since it invests mainly in stocks and equities, this type of mutual fund is regarded as having the highest risk (in comparison to other MF types). Still, it also has the potential for the highest gains over the long term (5 years or more).

2. Bond Funds

This mutual fund invests in various fixed-income instruments, including commercial papers, government securities, and Treasury notes. Investors choose Bond funds because they are less volatile (than other MF types) while still offering the possibility of capital growth and protecting their funds from inflation.

3. Balanced Funds

This kind of mutual fund has a portfolio comprising equities, bonds, and money market funds. It is regarded as the preferred fund type for investors with a moderate appetite for risk.

4. Money Market Funds

This kind of mutual fund mainly invests in corporate bonds and time deposits, which are short-term debt securities. Although it is thought to be the safest type of MF, it also offers the lowest rate of return on investment. For those seeking short-term investments, this is typically advised.

Mutual Fund Type Comparison

| Mutual Fund Type | Risk Type | Invests In | Goal | Investment Time Frame |

| Stock/Equity Fund | Aggressive | Stocks and Equities | Long-Term Capital Growth | 5 years or more |

| Balanced Funds | Moderate, Conservative and has a greater risk rating than Bond Funds | Combination of securities, bonds, and money market instruments | Medium to Long Term Capital Growth | 3-5 Years |

| Bond Funds | Moderate, Conservative | Fixed-income securities (such as government bonds and notes) | Stability combined with prudent capital growth | 1-3 Years |

| Money Market Funds | Conservative | Securities with a short maturity (time deposits, corporate bonds, cash assets, etc.) | Minimal Capital Growth combined with Stability | Less than 1 year |

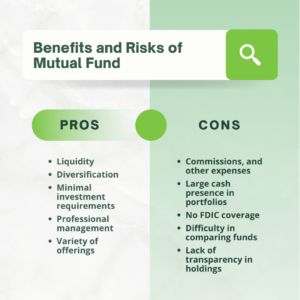

Benefits and Risks of Mutual Funds

Mutual funds provide expert investment management as well as potential diversification. Additionally, they provide three ways to make money:

Dividend Payments. Bond interest or equity dividends are two potential sources of revenue for a fund. After deducting costs, the fund distributes nearly all the income to the shareholders.

Distributions of Capital Gains. A fund’s securities could become more expensive. A fund gains capital when it sells security whose price has grown. The fund distributes these capital gains, fewer capital losses, to investors at the end of the year.

Increased NAV. The fund’s value and shares grow if the market value of the fund’s portfolio rises after subtracting expenses. Your investment has a more considerable worth, reflected in the higher NAV.

There is some risk associated with every investment. The danger of losing some or all of your investment in mutual funds exists because the value of the securities held by a fund may decline. As market circumstances change, dividends or interest payments may also alter.

Because previous performance can not indicate future returns, a fund’s past performance is not as significant as you believe. However, past performance shows a fund’s steady or erratic over time. The risk of an investment increases with fund volatility.

Buying and selling mutual funds

Instead of purchasing mutual fund shares from other investors, investors purchase them directly from the fund or through a broker for the fund. Investors must also pay purchase-related costs, such as sales loads and the mutual fund’s per-share net asset value.

Shares of mutual funds are “redeemable,” which means investors can sell them to the fund anytime. Typically, the fund has seven days to provide you with the money. Read the prospectus carefully before investing in mutual fund shares. You can find the information on the mutual fund’s investment goals, risks, performance, and costs in the prospectus.

Understanding costs

A mutual fund has expenses, just like any other firm. Funds pass these costs through by levying fees and charges on investors. Each fund has a different set of fees and expenses. For a fund with high costs to produce the same returns for you, it must outperform a fund with low prices. Over time, even slight variations in fees might result in substantial variations in returns.

Example:

For instance, you put Php 10,000 into a fund with a 10% annual return and 1.5% yearly running fees. You would have around Php 49,725 after 20 years. After 20 years, if you invested in a fund with identical performance and 0.5% fees, you would have Php 60,858.

How do Mutual Funds Work?

There are two ways that stock and bond funds can profit:

- The fund must pay out dividends and interest to its shareholders when the underlying security it invests in pays them.

- Capital Gains. A fund makes money when it sells underlying security for more than it originally paid. The fund realizes a “net capital gain” and is compelled to transfer that gain to its shareholders when its profits surpass its total losses.

Then, how do you make money as an investor?

- When the fund distributes income or capital gains to you.

- When you sell your fund shares for a price greater than what you paid when you first purchased them.

How do payouts from mutual funds operate?

Distributions may take the form of “taxable dividends,” capital gains, interest income, or income from overseas sources. Mutual funds can generate revenue from dividends on stocks and interest on bonds kept inside the fund’s portfolio since they invest in various assets. A fund will typically distribute to fund owners a percentage of the money it earns over the year. Additionally, most funds will distribute their profits to investors in the form of distributions if they sell securities whose prices have increased.

Finally, the price of the fund’s units will rise if a fund’s Net Asset Value (NAV) increases in value without being sold by the fund manager. Then, investors can resell their mutual fund units on the open market for a profit. Regardless of whether they are paid out in cash or reinvested into the mutual fund, distributions are typically taxable to the investor.

How exactly are distributions determined?

Distributions are made to unitholders proportionately to the number of units they held on the “record date,” which is when distributions are calculated.

The specific fund will determine the frequency of distribution payments, which may be made monthly, quarterly, or annually.

Where do Mutual Funds Invest?

- Bonds and other fixed-income securities are the primary investments of fixed-income funds, which are thought to be less risky than stocks or equities.

- Equity funds invest in the stock market to help your money increase over time.

- Multi-asset funds are made to produce returns by investing in various asset classes and adjusting assets on the fly over time.

Asset allocation funds provide a balanced portfolio by helping to manage risk and traverse various market conditions. Growth-oriented mutual funds also exist.

Best Mutual Funds in the Philippines

Due to their concern about being scammed, many Filipinos are apprehensive about investing in mutual funds. However, you can use the company lists on the SEC website to search for a reputable company.

The best mutual fund companies in the Philippines as of February 2022 are shown below:

| Mutual Funds Company | Fund Type | 1-Year Return (%) |

| Philequity Dividend Yield Fund, Inc. | Stock Funds | 23.28% |

| ATRAM Alpha Opportunity Fund, Inc. | Stock Funds | 23.04% |

| First Metro Save and Learn Philippine Index Fund, Inc. | Stock Funds | 11.76% |

| Sun Life Prosperity Dynamic Fund, Inc. | Balanced Funds | 11.49% |

| Philequity Fund, Inc. | Stock Funds | 10.37% |

| First Metro Save and Learn Equity Fund, Inc. | Stock Funds | 10.11% |

| First Metro Save and Learn F.O.C.C.U.S. Dynamic Fund, Inc. | Balanced Funds | 9.58% |

| Philequity MSCI Philippine Index Fund, Inc. | Stock Funds | 9.43% |

| First Metro Phil. Equity Exchange Traded Fund, Inc. | Exchange Traded Fund | 8.99% |

| Sun Life Prosperity Philippine Equity Fund, Inc. | Stock Funds | 8.94% |

What to Keep in Mind Before Starting Mutual Funds?

As you evaluate your mutual fund selections, care to take into account the following factors:

- Initial Investment: The least sum of money is required to create an account.

- Additional Investment: The smallest amount of money you can add to your portfolio.

- Front-end Fee: The portion of your investment that you pay the business as a fee.

- Management Fee: You will be charged a management fee each year to cover the cost of running a fund.

- Exit Fee: You will be charged an exit fee if you withdraw during the first several months.

- Investment Value: This refers to how much each share of the fund provided to investors is worth. It is the total of all funds less any outstanding debts. The number of shares is then divided by the outcome.

- Proof of Ownership: These are the shares that were issued to you. Your investment and the NAVPS determine how many shares you receive.

- Securities: Also known as stocks, bonds, or money markets, these are the assets that make up a fund.

- Earnings: These financial sums are exempt from taxation.

How to Create an Account for Mutual Funds?

Step 1. Visit the Mutual Funds website.

Visit the website of the mutual fund company of your choice.

Here are a few links to Philippine-based mutual fund companies that are authorized:

- Philequity Dividend Yield Fund, Inc.

- ATRAM Alpha Opportunity Fund, Inc.

- First Metro Save and Learn Philippine Index Fund, Inc.

- Sun Life Prosperity Dynamic Fund, Inc.

- Philequity Fund, Inc.

- First Metro Save and Learn Equity Fund, Inc.

- First Metro Save and Learn F.O.C.C.U.S. Dynamic Fund, Inc.

- Philequity MSCI Philippine Index Fund, Inc.

- First Metro Phil. Equity Exchange Traded Fund, Inc.

- Sun Life Prosperity Philippine Equity Fund, Inc.

Step 2. Registration

You will be required to answer a questionnaire to ascertain your risk profile after viewing the website of your chosen business. Additionally, you will be required to select the sort of mutual fund that best fits your risk tolerance and investing objectives.

Step 3. Forms and Documents

From their website, get the necessary paperwork. The prospectus, investor profile analysis, and application form are all included documents. The SEC mandates the prospectus as a document. It displays investment opportunities.

Step 4. Send in your requirements

Don’t forget to complete all the necessary paperwork. Visit the location of your chosen company’s nearest branch. Bring both original and photocopies of your valid identification. You can mail your documents if going to the branch’s location bothers you.

Step 5. Funding your Mutual Funds

You can begin funding your account as soon as you confirm it. Your initial mutual fund deposit must be between PHP 5,000 and PHP 10,000. Most investors enroll their mutual fund accounts in their bank’s online banking system for convenience, making it simple for them to transfer funds to fund their mutual funds.

Once a Mutual Fund account has been created, you may now begin purchasing or selling. You can now routinely check on the performance of your mutual fund; this could be done annually or every six months. It will also provide you with information on current investment methods.

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.