Financial, Fresh graduate, Young Adult

6 Starter Credit Cards for Credit Card Newbies

6 Credit Card Options that You Can Get If It’s your First Time

Adulting is a path that everyone is scared to take. A lot of responsibilities to take care of, including the obligation to be financially independent, and having a credit card is one of the best financial tools you can use. Being interested in applying for a credit card is a pain. It takes so much time to prepare all the needed documents, plus deciding which credit card to apply for takes a lot of consideration.

MINS TO READ: 8 minutes

AGE BRACKET: 18 – 25 years old

There are a lot of credit card offers in the Philippines that you can consider. There are many banks to start with, and many different types of credit card offers that the bank provides. Since you are a starter, you might be thinking about which credit card suits you best. You probably just started working and earning an average amount monthly. Therefore, I have listed all the Credit Card suitable for beginners. These credit cards offer a small amount or no annual fee, only requires a minimum wage a month, but still provide a lot of perks and rewards to enjoy using your credit card. But before going to the best part, here are some quick takes on deciding on your first credit card.

How to get approved on my credit card application?

Waiting for that call to know if your credit card application is approved or not is a bit stressful, especially if you’re not confident that you fit the qualifications needed to have a credit card. As a starter, that’s normal! I laid out some tips you can follow to ensure approval of your application.

1. Open a deposit account first.

Opening a deposit account and maintaining at least a ₱20,000 balance on your account will give the bank an idea that you are a qualified credit card holder. Strict banks that offer credit card usually checks the applicant’s bank accounts to see your cash and income flows. This is also an advantage if you plan to apply for a secured credit card. You can use your account as collateral for your credit card.

2. You must have a reliable and stable source of income.

Having a stable source of income is one of the qualifications every applicant should have. This assures the bank that they will be paid. Being in the same company for a long time increases your chances of being approved since it shows you are committed and loyal. This equates to the quality of a good payer, someone who’s reliable and punctual in paying the money you borrowed.

3. Choose a credit card that suits your financial situation

Applying for a credit card you can’t afford will be a mistake. Banks can see your cash flows and will know your income based on the requirements that you will pass. They will see if you can afford the credit card you’re applying for, and you will be rejected if you apply for a card that does not match your salary range.

4. Prepare all the documents needed and ensure that they are accurate and complete.

Planning and preparing for your credit card application may be a lot of work, but it is crucial to ensure that all required documents are accurate and complete. Always double-check all your papers before submitting them. One of the causes of delay and rejection in credit card applications is the incomplete required documents that the applicant passed, which causes inconsistencies in your application.

5. Avoid follow-ups on your application.

Continuous follow-ups on your application within two weeks would reflect poorly on you. This gesture shows the bank that you badly want and are greedy for credit. It is best to wait for the outcome and avoid frequent follow-ups on the bank within the first two weeks. If you do not receive any call or message from them, it is most likely that your application will be rejected.

How to choose the right credit card?

Remember that there is a lot to consider when choosing the right credit card for you. There is no perfect credit card. However, considering your spending habits and lifestyle may help you find a good match.

1. Low interest, low annual fee, or rewards card?

There’s a saying that you can’t have it all. The same applies to credit cards. Generally, you have to choose between these three depending on your budget and lifestyle.

- Low-interest card – credit card usually offers 2% monthly interest. However, some credit cards offer an interest lower than this. Having a low-interest credit card will help you if you can’t pay your balance in full as it will reduce the amount of interest your balance will again. But then again, leaving your outstanding balance for a long time is never recommended, even if your card offers low interest.

- Low annual fee card – annual fees vary depending on your card. Some cards offer an expensive yearly fee; some waive it off for the first year or even for life! It is best to see if you can afford to pay your annual fee if you opt for something that requires you to pay the fee. But then again, yearly fees are avoidable if your card offers reward points that you can convert into waiving your annual fee.

- Rewards card – this type of card makes your credit card experience enjoyable. You can earn reward points on every purchase, which vary on your card. Rewards can be in any form, such as air miles, cashbacks, or points you can redeem into gift certificates, travel vouchers, etc.

2. Features and Benefits

Other than the rewards offered and low annual fees or interests that the bank uses to entice people to apply, you should also see the card features and benefits that come with it when choosing. Some options that come with the credit card are the no balance transfer and over-limit fees, whereas some bank charges you an expensive fee for that. Aside from this, some banks’ credit cards, the plastic card themselves, come with a chip that protects your financial information. Even insurance and travel perks are included in some offers, which are an excellent benefit of having a credit card. You must check these out and compare to see which one suits you.

3. Terms and Conditions

Filipinos may not be fond of reading the terms and conditions, but it is vital to read them when applying for a credit card. Seeing how much interest you have to pay, all the fees you will be charged, and the conditions of having a credit card, you should know it is a must. Being a credit card holder comes with great responsibility that you must take care of, and understanding its terms and conditions is vital. Knowing as much as possible about the credit card you’re applying for and will have once you are approved may save you from a potential hassle.

Credit Card for Starters

AUB Classic Mastercard

The AUB Easy Mastercard offers a flexible credit card payment that you can choose from once a month, twice a month, or even weekly payments! You can also decide how much you will pay depending on your budget or how much you can afford to pay on your chosen payment date. This is also the best pick for starters since there is no annual fee and offers no interest on new purchases.

Features and Benefits

- No interest in new purchases

- Freedom to choose when and how much you want to pay

- It comes with a supplementary card that you can enroll as many as you want with no annual fees to pay

- Offers a credit limit that ranges from ₱40,000 – ₱90,000 depending on your hold-out deposit

- Earn one reward point for every ₱50 purchase that you can redeem into airline miles, travel vouchers, e-gift certificates, and cash back.

- Rewards accumulated do not expire

Fees and Charges

- 2% monthly interest rate

- No annual fee

- A late payment fee of ₱1,000 (monthly), ₱500 (semi-monthly), or ₱250 (weekly) varies on your payment option or your unpaid minimum amount due, whichever is lower.

- A temporary Credit Limit increase fee of ₱300 for every request

Application Requirements

- You must be at least 21 years old

- Gross monthly income of ₱21,000

- A regular employee for at least one (1) / has a registered business operating for at least one (1) year.

- Must have an active mobile phone and email address

- Government-issued ID

- Proof of income documents

Computation / Comparison

AUB Classic Mastercard allows you to choose when and how much you would like to pay with various options. For Instance, you choose monthly payment, where you can select your due date from the 1st to the 30th day of the month, with a minimum amount due of ₱4,000, where you can choose between ₱4,000 – ₱9,000.

Suppose your balance is ₱8,000 with 2% interest. Thus, multiply your balance by your interest rate to have your interest amount (8,000 x 0.02 = 160). Therefore, you have a ₱160 interest charge on your total balance, and you have to pay ₱8,160 on your payment due date. However, since you chose ₱4,000 as your minimum amount due, you have to pay at least ₱4,000 on your chosen payment due date. Plus, suppose you pay your dues late; you have to pay a late payment fee of ₱1,000. To sum it up, you have to pay ₱9,160 (₱8,160 month’s payment and ₱1,000 late payment fee) if you pay your balance late. In cases where you have to request a temporary credit limit increase, the bank will also charge an amount of ₱300 on your monthly payment.

In addition, this credit card does not offer a cash advance feature, which makes other credit cards better than this one if you opt to withdraw money from your credit card in an emergency.

Citi Simplicity+

Citi Simplicity+ is considered the top choice for starters who want a credit card. It allows you to have the best experience using your credit card without worrying about credit card fees since it offers no late payment fee, no over-limit fee, and no annual fee for life! It’s straightforward yet affordable to own and easy to qualify.

Features and Benefits

- 10% interest back if you pay at least the minimum due on or before your payment due date.

- Exclusive dining deals and promotions

- Year-long exclusive privileges and promos on different merchants

- Deals and discounts locally and internationally

- You can apply for up to 7 supplementary cards where you can earn points, miles, and rebates from their purchase with no annual fee

- Allows you to get emergency cash with your credit card

Fees and Charges

- 2% monthly interest

- No annual fee for life

- No late payment fees

- No over-limit fees

- Cash Advance service charge of ₱200 per transaction

Application Requirements

- You must be at least 21yrs old

- Gross monthly income of at least ₱21,000

- Must have an active mobile number or landline

- Photo-bearing government-issued ID

- Proof of income documents

Computations / Comparison

The 10% interest back on interest charges is one of Citi Simplicity+’s benefits, where you only have to pay at least your minimum due amount on or before your payment due date. Suppose you have a balance of ₱8,000 with an interest charge of 2%. Based on the first computations above, you will earn an amount of ₱160 interest on your balance with a month’s payment balance of ₱8,160.

If you pay your monthly payment balance or at least your minimum due amount, you will receive a 10% cash rebate. To compute this, multiply your interest charge by 10%. Thus, in this case, 160 x 0.10 = 16. Therefore, you will receive an amount of ₱16 cash rebate for paying your dues on time.

Metrobank M Free Mastercard

You don’t have to be bothered with annual fees since, with Metrobank M Free Mastercard, yearly fees are waived for life! Applying for M Free Mastercard made it easy with a low minimum income requirement. It is a considerable benefit for young adults who want their first credit card.

Features and Benefits

- Credit Card has an embedded chip card that protects you from fraud credit card cloning

- 0% installment program from different merchant establishments

- You can enroll for a supplementary card with no annual fee.

- A contactless card that allows you to pay on any card terminal that has a contactless symbol

Fees and Charges

- 2% monthly interest rate

- No annual fee

- Late payment fee of ₱1,000 or the unpaid minimum amount due, whichever is lower.

- An over-limit fee of ₱750 per occurrence

- A cash advance fee of ₱200 per transaction

Application Requirements

- You must be at least 21 yrs old

- A gross monthly income of ₱15,000

- Must have a Tax Identification Number (TIN) and SSS/GSIS No.

- Must be at least six months employed as a regular employee

- Photo-bearing government-issued ID

- Active mobile number number or landline

- Proof of income requirements

Computations / Comparison

The Metrobank M Free Mastercard does not have that many features and benefits aside from the 0% installment program, and no annual fee offers. Like other credit cards, it provides a 2% monthly interest rate. The exact monthly computation applies to this credit card. However, in terms of over-limit fees, this is much more expensive than the before-mentioned credit cards.

This credit card is not much, but if you just want a credit card that you can use for daily necessities and emergencies, this is not bad and will still be a good choice since you don’t have to pay annual fees. Plus, the chip card embedded in your card greatly protects your financial information and fraud.

PNB Classic Visa

PNB Classic Visa is one of the credit cards that you can also consider since it only offers you a low amount for your annual fee and only requires a monthly income of ₱10,000. One thing to be drawn into are the insurances that come with it, which will be a lot of help since this can be your first credit card.

Features and Benefits

- Enjoy a 1% rebate on your revolved interest.

- Pay your purchases in Peso even when you’re abroad

- A supplementary card that you can apply for with no annual fee for life

- It comes with a Free Purchase Protection Insurance that covers up to ₱250,000 annually in cases of accidental damage and theft of your purchases within 90 days.

- It comes with Travel Insurance that covers up to ₱1M when you charge your travel fare on your credit card, covering lost luggage and flight delay.

- It comes with Fraud Transaction Insurance that covers up to ₱250,000 for only ₱120/year in cases when your card is used in fraudulent transactions.

Fees and Charges

- 2% monthly interest rate

- ₱300 annual fee, waived for the first year

- Late payment fee of 7%(Peso) or 5%(Dollar) of the unsettled minimum amount due

- An over-limit fee of ₱300 or US$10

- A Cash Advance fee of ₱200 for Pesos and US$4 for Dollars.

Application Requirements

- You must be at least 21 yrs old

- A gross monthly income of ₱10,000

- Photo-bearing government-issued ID with signature

- Proof of Billing

- Proof of Income documents

Computations / Comparison

Just like the Citi Simplicity+, the PNB Classic Visa offers a 1% rebate on your revolved interest. To compare both cash backs, Citi Simplicity+ 10% rebates are much higher than what the PNB Classic Visa offers. To see the difference, suppose we use the same computations above of having an ₱8,000 balance with a ₱160 interest charge. We can multiply the interest charged by the percentage offered to see how much cashback we can earn. Thus, 160 x 0.01 = 1.6. Therefore, you can earn an amount of ₱1.6 rebate when you pay your payment or at least your minimum amount due on or before your due date.

In addition, PNB Classic Visa requires you to pay an annual fee of ₱300, which is not that expensive and still a fair amount since the fees are a bit cheaper than others. For instance, your late payment fee only requires you to pay 7% of your minimum amount due. To compute your minimum amount due, multiply your total amount due by 3%. If your total amount due is ₱8,160 (including interest charge), thus 8,160 x 0.03 = 244.8. Since ₱244.8 will be your minimum amount due, your late payment fee will be 7% of ₱244.8. Thus, 240 x 0.07 = 17.14. Therefore, your late payment fee will be ₱17.14. A lot cheaper than other credit cards.

PNB Ze-Lo Mastercard

This PNB Ze-Lo Mastercard is also a promising startup if you want to have your first credit card that you can use for your daily spending. Like other credit cards mentioned above, it also comes with no annual fee for life. Also, you do not have to pay fees in some occurrences and offer lower interest rates, which is a big help if you want to spend less and save money.

Features and Benefits

- You can apply for up to nine (9) supplementary cards and enjoy a free annual fee for life.

- Pay your purchases in Peso even when you’re abroad

- It can be used as a contactless payment

- 3% rebate on fuel purchases made at participating Caltex stations

Fees and Charges

- 88% monthly interest rate

- No annual fee for life

- No late payment fees

- No over-limit fees

- A Cash Advance fee of ₱200 for Pesos and US$4 for Dollars.

Application Requirements

- You must be at least 21 yrs old

- A gross monthly income of ₱10,000

- Photo-bearing government-issued ID with signature

- Proof of Billing

- Proof of Income documents

Computations / Comparison

Of all the starter credit cards mentioned, PNB Ze-Lo stands out in its 1.88% monthly interest rate offer and no annual, late payment, and over-limit fees. This makes it best for starters who need a credit card solely for emergencies and necessities. To compare its huge difference on other credit cards in terms of interest rate, we can compute the interest that will be charged on you suppose you have an ₱8,000 balance. Thus, 8,000 x 0.0188 = 150.4. Therefore, your monthly payment will be 8,150.4, a ₱9.6 lower than other credit cards.

Given the cheap fees and interest, PNB Ze-Lo does not reward you as much as other credit cards other than your fuel purchase on selected Caltex Station, which rewards you a 3% rebate. Suppose you purchased an amount of ₱2,000 on fuel; your rebate will be 2,000 x 0.03 = 60. Therefore, you will earn an amount of ₱60 cash rebate on your purchase.

RCBC Bankard and Flex Visa

Spending made it fun with RCBC Bankard and Flex Visa! You can earn 2x reward points on your purchases and benefit from the insurance that it came with. The financial flexibility that you can flex to everyone. The annual fee may be a bit pricey, but you can avail their promo of no annual fee for life. To read more about this promo, visit here.

Features and Benefits

- Earn reward points on your spending

- Get 2x rewards on your preferred categories (Dining, Clothing, Travel, or Transportation) and switch your chosen categories in every billing cycle.

- Redeem your accumulated points for shopping vouchers, cash rebates, cash credit to your deposit account, or even as a donation to your chosen charity

- You can redeem free flights using your accumulated points by enrolling in the Airmiles program.

- It comes with Travel Insurance and Purchase Protection when you charge your travel purchases on your credit card

- The benefit of enjoying the comfort and luxury of airport lounges while you wait for your flight

- 0% installment rate on all your purchases abroad

- The power to spend by the bonus travel limit that you need whenever you travel

- The card is embedded with EMV Chip Technology to increase security and avoid fraud.

- It comes with Credit Protect Plus, which protects your financial information.

Fees and Charges

- 2% monthly interest rate

- ₱1,500 annual fee; waived for the first year

- Late payment fee of ₱850 / US$17 or the minimum amount due, whichever is lower

- An over-limit fee of ₱600/US$12 is charged once within the statement cycle.

- A cash advance fee of ₱200/US$4

Application Requirements

- You must be at least 21 yrs old

- A gross monthly income of ₱15,000

- Government-issued valid ID

- Must have a mobile number and a landline at work

- Proof of income documents

Computations / Comparison

Having RCBC Bankard and Flex Visa as your credit card will be your biggest flex. As you can see, RCBC Flex Visa has the most benefits that you can have compared to other credit cards. However, it requires you ₱1,500 annual fee and is a bit expensive. In terms of monthly interest rate, it offers you the same rate as others. If you opt for a credit card with total rewards, I suggest this will be your best choice if you have the budget to pay all the credit card fees, which are avoidable in some cases.

Comparing Credit Cards

Reading each credit card’s features and charges may be time-consuming and confusing. It is hard to compare them and choose which you prefer best. With that, I have prepared a table of the credit card benefits and their fees so you can compare them and decide better which is best and suitable for you.

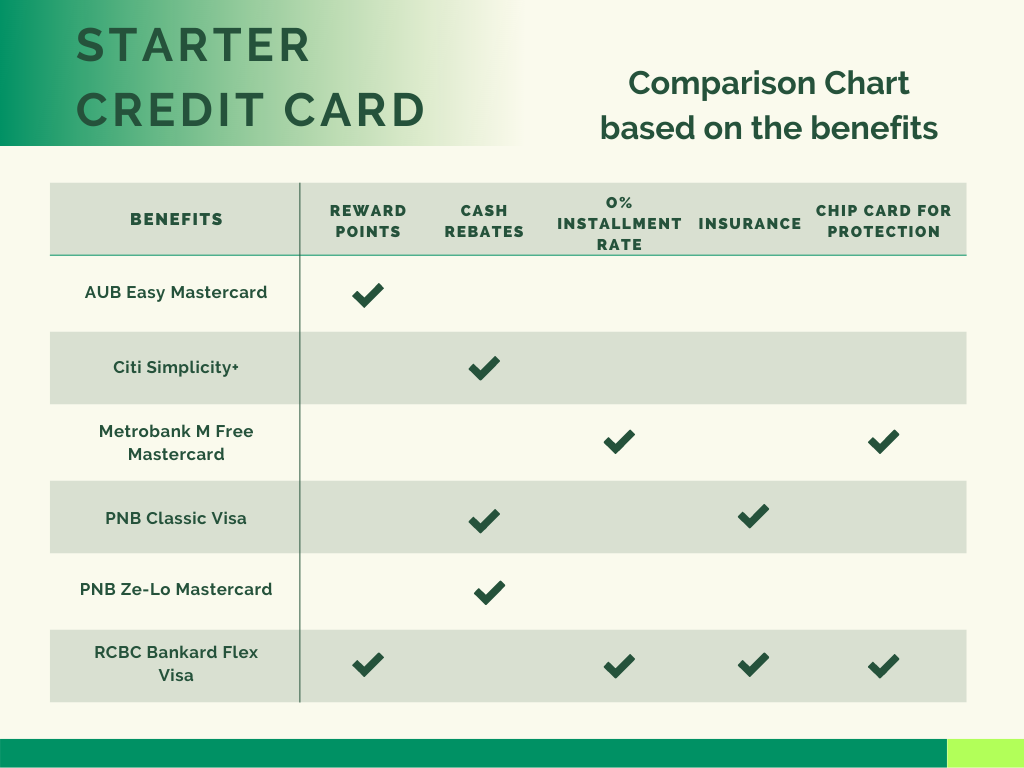

Comparison between Credit Card Benefits

I have compared them based on the benefits each credit card offers. They are compared based on the reward points that you can earn, cash rebates on your purchases, a 0% installment rate, different insurances provided, and a chip embedded in your card for your financial protection. Each of these benefits is beneficial in having a credit card and one thing you should consider in getting one. These are must-haves if you are planning to get a credit card. Therefore, in the table provided, you can see each credit card’s benefits, where you can easily choose which one you prefer based on the benefits that suit you most.

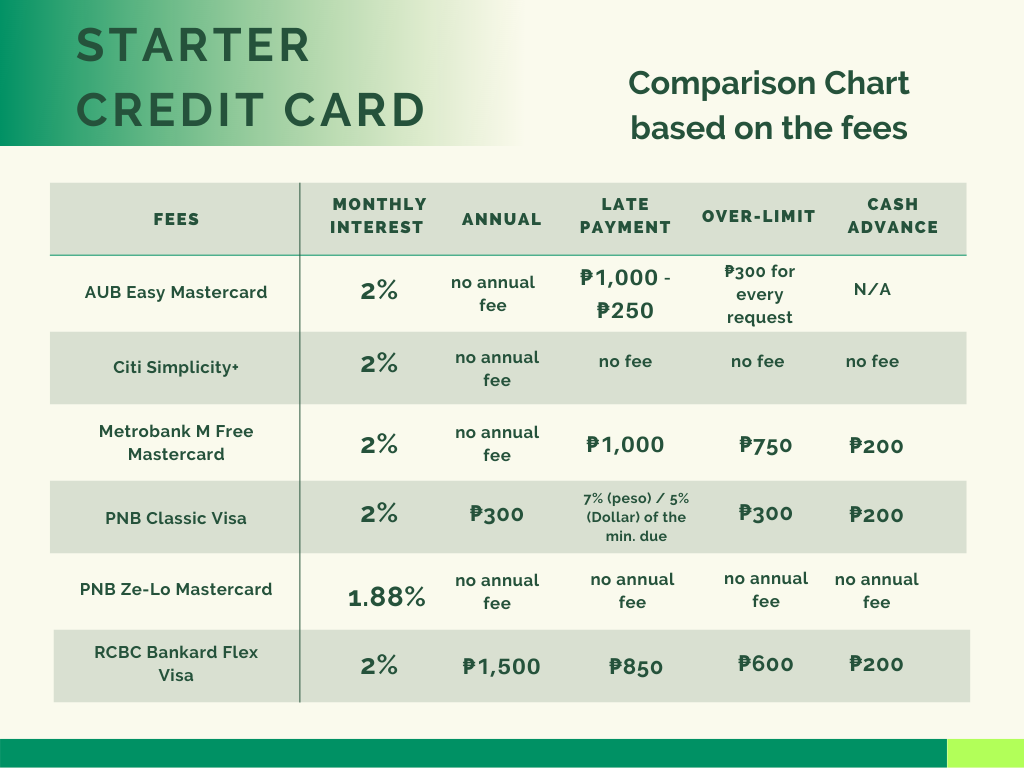

Comparison between Credit Card Fees

This table of fees for each credit card allows you to see which will be best if you are eyeing something that will help you spend less and save more. Most credit cards offer no annual fees, and some have a yearly fee. We can see that the credit cards that provide payments usually have more benefits, as you see in the other table. However, focusing only on the fees will be enough if you prefer to spend less than benefit from the rewards.

Suppose you’re still confused about what credit card you should choose; better to look at the comparison tables closely and see which will suit you. If you want to have a credit card where you can earn some rewards and benefit from the perks, it is suggested to look at the first table. If you’re more into saving and just got a credit card for daily uses and purchases, it is better to focus more on the second table. But, if you prefer both rewards and want to spend less, it is best if you analyze the tables and determine which one is for you.

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.