No products in the cart.

Financial

The Ultimate Guide to Boosting Your Credit Score for Financial Success

Credit Score in the Philippines

You’ve probably already daydreamed about leading an independent life and wondering when you’ll get there. There’s a good chance that you’ve told yourself that by a given age or stage in your life, you would’ve accomplished something.

Even though you have the cash to buy some of the things you desire, it is still preferable to pay for them in installments rather than all at once to keep your finances on track and to have that wonderful cash flow that could cover your other wants and requirements. In this manner, you may be certain that you are moving in the direction of financial stability.

Mins to Read: 17 minutes

Age: For all

What is a credit score?

Your credit score is often a three-digit number that assesses your likelihood of repaying a loan. From the time you first established a bank account, applied for a credit card, and started applying for loans, it includes a variety of financial data about you. All of your credit accounts, including inactive and active credit lines, are also included.

But why is having a high credit score significant? primarily because in many important financial situations, credit scores serve as your financial scorecard that evaluates your reputation. It serves as the foundation for the approval of all loan and credit card applications by banks, credit card firms, and other lending organizations. It also depends on other things, such as the number of accounts you have that are in good standing and your ability to make timely payments.

This would not apply to all lenders, banks, and credit companies, though, as there are different methods that official financial institutions in the Philippines determine credit scores.

You might perhaps not understand it. While managing your finances and banking, you may have come across the concept of credit scores. It may appear to be a harmless figure at first, but it actually has a lot of influence, particularly if you’re considering applying for a loan, a credit card, or other types of credit accounts.

Let’s get straight to the point and discuss what credit scoring actually is in the Philippines, how it works, and what you should consider doing to improve your credit score. We’ll also be discussing some other financing options without a credit history or score! So in with an open mind and continue reading here

How can I check my credit score in the Philippines

A government-owned and controlled corporation (GOCC) in the Philippines gathers credit data from a variety of sources, including banks, financial institutions, insurance companies, financing companies, credit cooperatives, utility companies, and other businesses that provide loans. To assist creditors in determining a potential borrower’s capacity to pay, the CIC gathers all relevant data about them. You have a choice between applying for your credit score through the CIBIApp web tool or physically requesting a credit report from CIC.

Furthermore, only people having credit records or transactions to financial institutions engaged in credit-related activities are authorized to access their credit reports and scores given the current state of the credit information exchange system in the Philippines. Because of this, you should be cautious about whether you’re paying payments on time or not if you’re new to monitoring your credit score.

How to obtain your credit history in the Philippines via CIC

Here are the procedures you must follow to submit a credit report request on the CIC website in order to obtain a copy of your CIC credit report:

✅Select “Services.”

✅Choose “Get a CIC Credit Report” from the menu.

✅Before clicking the “I accept” button, carefully read the Terms & Conditions.

✅Select the appointment date that works best for you.

✅Give the necessary private information.

✅Print your application form after downloading it.

For an in-person credit score check using a credit report, go to the CIC office in Legaspi Village, Makati City, Philippines. The CIC uses a Know Your Customer (KYC) procedure to make sure your credit information is secure.

How much does it cost to request a credit report with a credit score? CIBI charges ₱235 for the credit report with a credit score.

What is a Good Credit Score?

In the Philippines, a credit score can vary from 300 to 850, with 850 being the best possible number. The higher your credit score, the better.

- Excellent: 750 to 850

- Very Good: 700 to 749

- Fair: 650 to 699

- Poor: 600 to 649

- Bad: 300 to 599

How often is the credit score updated? The credit score is calculated at the time of request or inquiry, based on the current information presented in the credit report. Participating entities must submit regular updates on their borrowers’ credit data within 30 days of being available.

Can OFWs and migrant workers access the CIBIApp? Yes. The CIBI App can be accessed anytime and anywhere via mobile or desktop. You can also use the CIBIApp to request your credit report online, but first you must go through a character verification process that involves an online call with a company verifier.

Is it possible to have no credit score? Yes. No credit score can be generated if you do not have any credit or loan transactions in your credit report within the last two years. You must have a history of past credit accounts, including loans and credit cards, in order to have a credit score.

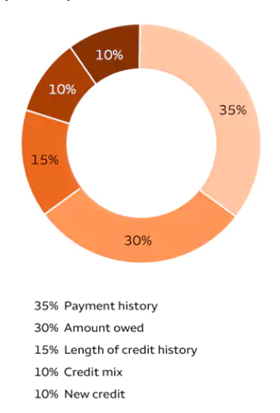

What Influences Your Credit Score?

You must take into account these 5 elements to improve your credit score

- Payment history – This is the most evident factor, based on your track record of timely and regular debt repayment. Did you know that your credit score might decrease by 90 to 100 points if you skip a payment cycle?

- Duration of credit history – This is determined by the number of years you have held credit cards or loan accounts. Do you have credit cards? The oldest, newest, and all other cards you have in your wallet will be averaged to determine the age.

- Utilized credit types: Do you have a variety of credit accounts, such as mortgages, credit cards, cash advances, and loans for a car or other object? This may be examined by lenders to determine your ability to manage all of these accounts.

- Amount Owing – The entire amount you presently owe on all of your credit accounts, including credit cards, is known as the “amount owing.” You are less likely to be granted approval for additional loans or credit accounts the more debt you have or the greater the amount you owe.

- New Credit – All of your recent applications for credit cards, loans, and the like are referred to as new credit applications. Be cautious about applying for many credit accounts at once because it can lower your score.

How do lenders compute your credit score?

What Does Not Influence Your Credit Score?

It’s important to understand that your credit score simply represents the details of your credit report. Your lender’s appraisal may take into account additional data. Your age, present salary, or tenure of employment, for instance, are not shown in your credit report. It is equally crucial to be aware of the following elements that have no bearing on your credit score:

- Income: Although it doesn’t directly affect your credit score, the quantity and fluctuations in your income can nevertheless be taken into account by the bank when issuing loans.

- Bank accounts without credit (checking, savings, investment, debit accounts)

- Personal Information (education level, age, gender, religion, political party, marital status)

- Credit history of the spouse: When two people get married, their credit histories are not pooled when calculating credit scores, which are based on an individual’s credit history.

- Payments for utilities, telco, and small businesses that aren’t submitting entities recognized by the credit registry won’t be included in your credit report and won’t have an impact on your credit score.

- Checking your credit reports – repeatedly obtaining your credit report will not lower your credit score.

- Additional authorized users on your credit card will not have an impact on your credit score as long as you are able to make your regular monthly payments.

What distinguishes a credit score from a credit report and a credit history?

- A borrower’s credit score is a number that represents the statistical likelihood that they will be able to repay their obligation. Because it only shows one’s financial standing at one particular point in time, it is known as a “snapshot of a credit report.”

- A credit report is a written record that provides detailed information about the previous and ongoing financial dealings of a person or business. As it describes the credit accounts, payment history, and other personal or company information, it provides insight into what factors contributed to the credit score.

- A person’s credit history shows how they handled previous credit accounts. It displays the total number of credit lines held, the opening date, the loan amounts, and the promptness of payments. Negative information such as missing payments, bankruptcy filings, and loan defaults are also included. The credit report contains information on these things.

Lenders use these documents to determine loan terms and approve a new credit line. You now know the distinction between a credit report and a credit score. Regularly keep an eye on both, ideally prior to making a credit card or loan application.

Tips and Warnings

1. As soon as you can, establish good credit. Reviewing your credit record and checking your credit score is the first step.

2. You may raise and keep your credit score high by doing the following:

- Be accountable for your financial responsibilities; settle accounts completely and on schedule.

- Inaccurate information on your credit report should be updated or corrected as it may influence your credit score.

- Don’t take on any more debt.

- Even if you aren’t using a credit card, it is best to keep it open because doing so could increase your credit utilization rate.

- Ask your credit card company to raise your credit limit, but don’t use it all at once. This enables you to keep your credit use rate low.

3. Advantages of a good credit score

- quicker loan and credit card application acceptance

- greater credit card limits, reduced interest rates, and increased loan amounts

- lower premiums or payments each month

- Lower security deposits required for leases

- reduced insurance costs

- gaining access to a larger range of financial goods or services

- Benefit from premium credit cards with stronger incentives and benefits.

- ability to renegotiate loan terms

- Spend less now and more later

- Establish a solid reputation in the eyes of future employers that review credit reports as part of their background checks.

4. There are several scoring systems and requirements used by banks and lending organizations.

Being turned down for one credit facility does not ensure that you will be turned down for another.

5. Keeping your bills from being sent to collection agencies.

When a collection agency takes care of these invoices, even if they weren’t initially on your credit report, they will now be included and will have an impact on your credit score.

In this manner, you may be certain that you are moving in the direction of financial stability.

It is typically practically standard practice to seek for a loan or credit from a financial institution when this occurs. When you simply have to pay the bank or lending firms in installments, plus interest depending on which bank you approach, this allows you more financial flexibility. Sounds practical?

Even if it seems like an excellent and simple option to get the loan you’re searching for, you still need to pass a credit inquiry in order to be considered for one. Having a very good credit score is the one requirement you must meet in order to pass the investigation.

Now you know what exactly is credit score, nothing can stop you now. Keep up!

MUST-READ AND SHARE!

2023 Your Practical Wedding Guide

Your Ultimate Access to Kuwait Directories in this COVID-19 Crisis

Investments and Finance Ultimate Guide

OFW FINANCE – Money News Update that you need to read (Table of Contents)

A Devotional for having a Grateful Heart

Stock Investment A Beginner’s Guide

How To Save Money Amidst Inflation

Philippines Best Banks with High-Yield Savings Return

Essentials Before Applying For a Credit Card

Credit Card Starter Guide for Beginners

If you like this article please share and love my page DIARYNIGRACIA PAGE Questions, suggestions send me at diarynigracia @ gmail (dot) com

You may also follow my Instagram account featuring microliterature #microlit. For more of my artworks, visit DIARYNIGRACIA INSTAGRAM

Peace and love to you.